There are several recent factors affecting false positives in derivative transactions. First, the past 90 days have seen higher than average expirations.

The variance for currency hedging data across 4 major asset managers remains above the 2 year benchmark averages. This makes currency errors less predictable.

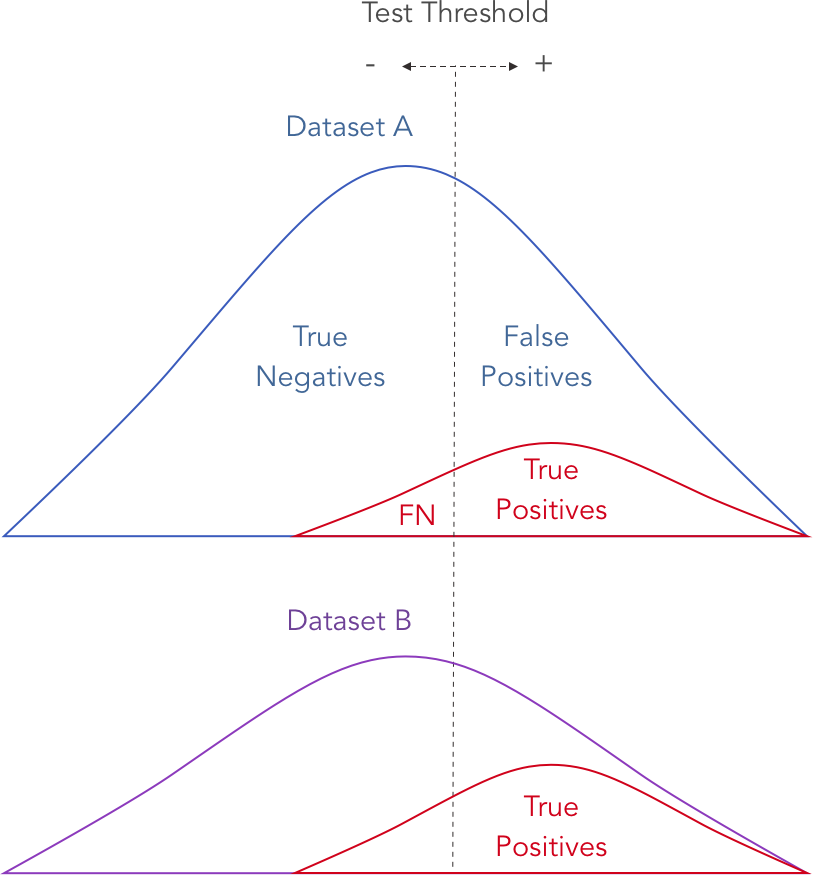

The March correction reduced the error rate as a percent of the total distribution to only 1%, As you can see in Dataset B, which excluded the outlier trading days owing to the correction, the false positive rate for the threshold is significantly reduced.

Our work in assessing data and applying algorithms to reduce time and increase error detection continues. We have worked principally in the NAV area where errors frequently occur due to processing window error and manual entry errors.

However, we have found that removing the obvious outlier trading days in datasets has materially lowered false positive rates.

We also believe that a better case tracking method is needed to identify the performance issues with fund administrators in eliminating errors. This work requires a persistent and skeptical algorithm that follows through like a detective.

OnCorps LLC

116 Huntington Avenue

Boston, Massachusetts 02116